Why is the sales budget the starting point for master budget?

What are Sales and Production Budgets? Preparation of the master budget starts with a sales budget. The sales budget guides the rest of the budgeting process because the level of production, and therefore the cash needed for production, is directly dependent on the level of sales forecast.

What is the starting point of the master budget process?

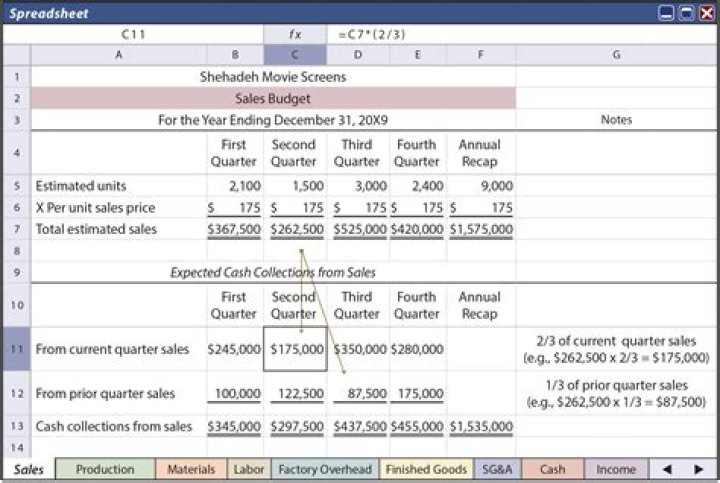

Question: The sales budget is the starting point for the master budget, as shown in Figure 9.1 “Master Budget Schedules”. What is a sales budget, and how is it prepared? Answer: The sales budget is an estimate of units of product the organization expects to sell times the expected sales price per unit.

Why is the sales budget the most important component of the master budget?

Answer: The sales budgetAn estimate of units of product the organization expects to sell times the expected sales price per unit. is an estimate of units of product the organization expects to sell times the expected sales price per unit. This is perhaps the most important budget as it drives most of the other budgets.

Why is the sales forecast so important in developing the master budget?

The master budget will offer guidance to every department in the company, knowing, starting at the sales forecast, where product needs to be priced, how to manage floor space and staff each step of the process. Having accurate sales figures is the key to the entire budgeting process.

What is the order of a master budget?

The production budget is needed to figure out direct materials, direct labor and manufacturing overhead budgets. Once these are all done, then comes the finished goods inventory budget. Once all of these budgets are done, we can do a cash budget, income statement and balance sheet to finish off the process.

Which element of a master budget is always prepared first?

Operating budgets are interrelated and a sales budget is always prepared first. (cont.) A cost of goods manufactured budget is a detailed plan that summarizes the estimated costs of production during an accounting period.

Which is not Section of cash budget?

There are some non-cash expenses that are not contained in cash budgets because they do not entail a cash outlay, for example, bad debts and depreciation. The cash outflow section in cash budgets contain: Planned cash expenditures. Fixed asset purchases.

What budget is always prepared first?

sales budget

Operating budgets are interrelated and a sales budget is always prepared first. (cont.) A cost of goods manufactured budget is a detailed plan that summarizes the estimated costs of production during an accounting period.

What are the four sections of a cash budget?

The cash budget typically consists of four major sections: (1) receipts section, which is the beginning cash balance, cash collectionsfrom customers, and other receipts; (2) disbursement section comprised of all cash payments made by purpose; (3) cash surplus or deficit section showing the difference between cash …