Why is the interest rate of a loan one of the most important things to consider Brainly?

Why is the interest rate of a loan one of the most important things to consider when shopping around for loans? The interest rate can drastically change the total amount paid to the lender, in the case of mortgages, up to thousands of dollars.

Why is the rate of the interest on the loan important?

The interest rate is the cost of debt for the borrower and the rate of return for the lender. Risk is typically assessed when a lender looks at a potential borrower’s credit score, which is why it’s important to have an excellent one if you want to qualify for the best loans.

What is the most important thing to consider when shopping for a loan?

Your current financial situation. When you’re considering applying for a loan, the most important factor in deciding whether to borrow money is you. Looking at monthly and yearly budgets may help you understand just how much you can afford to make in loan payments, thus helping you decide on a loan amount.

When choosing a loan is it more important to consider the length or interest rate of the loan Why?

A longer term length means lower monthly payments, but higher interest costs in the long run. To keep the cost of the loan down, you should look for the shortest loan term you can get while still keeping monthly payments manageable. The term length isn’t the only factor to consider when applying for a personal loan.

Does a loan need an interest rate?

Minimum-interest rules refer to a law that requires that a minimum rate of interest be charged on any loan transaction between two parties. For example, lenders can be charged tax on the amount of interest the IRS believes they should have collected on a loan, even if they didn’t collect any interest.

Why is it important to know the interest rate when borrowing money?

The interest rate is essentially how long you have to pay off your loan, and the shorter the better. The interest rate can drastically change the total amount paid to the lender, in the case of mortgages, up to thousands of dollars. d. The interest rate does not change, even between banks, so choosing the right time to borrow is essential.

What’s the best way to compare loan rates?

For some loan types, comparing interest rates is appropriate, but the APR is a better number to review. The APR factors in fees, including points and origination fees, while the interest rate is just the basic interest charged.

Is it better to ignore the interest rate on a mortgage?

The interest rate should be ignored, because there’s nothing a consumer can do to change it. b. The interest rate is essentially how long you have to pay off your loan, and the shorter the better. The interest rate can drastically change the total amount paid to the lender, in the case of mortgages, up to thousands of dollars.

What’s the interest rate on a consumer loan?

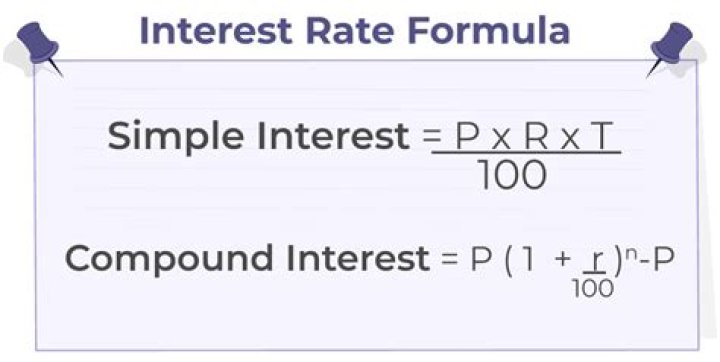

Loan R has a principal of $17,550, an interest rate of 5.32% (compounded monthly), and a duration of seven years. Loan S has a principal of $15,925, an interest rate of 6.07% (compounded monthly), and a duration of nine years.