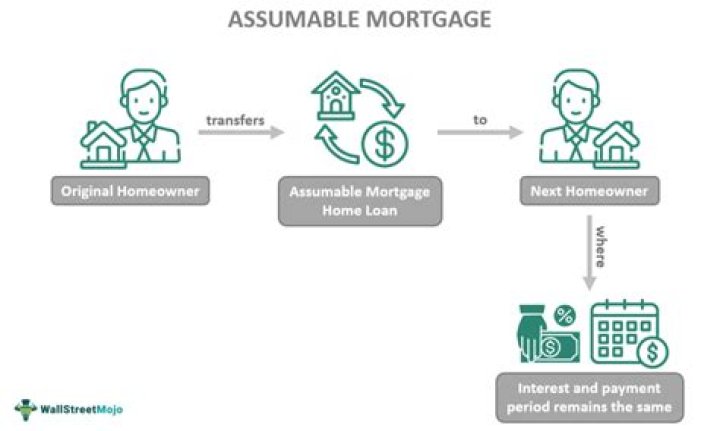

What makes a mortgage assumable?

An assumable mortgage is an arrangement in which an outstanding mortgage and its terms can be transferred from the current owner to a buyer. When interest rates rise, an assumable mortgage is attractive to a buyer who takes on an existing loan with a lower rate. Buyers must still qualify for the mortgage to assume it.

What are the advantages of an assumable mortgage?

Advantages. If the assumable interest rate is lower than current market rates, the buyer saves money straight away. There are also fewer closing costs associated with assuming a mortgage. This can save money for the seller as well as the buyer.

How do I know if I have an assumable mortgage?

1) Find Out If the Loan is Assumable You can check the loan documents to see whether assumptions are permitted. The loan document will typically state whether or not the loan is assumable under the “assumption clause.” The terms may also appear under the “due on sale clause” if loan assumption isn’t permitted.

Do you have to qualify for an assumable mortgage?

Unless you’re assuming a loan from a relative, you generally must qualify for mortgage assumption — once the home seller confirms they have an assumable loan. Generally speaking, the buyer must meet the same credit and income requirements applicable to a brand-new loan.

There are advantages for both the buyer and the seller when processing an assumable mortgage and taking over the seller’s loan, especially if the seller’s mortgage interest rate is much lower than the current market rates, or is lower than the rate the buyer might be able to get based on credit history.

What does it mean when a loan is not assumable?

Not assumable means that the buyer cannot assume the existing mortgage from the seller. Conventional loans are non-assumable. Some mortgages have non-assumable clauses, preventing buyers from assuming mortgages from the seller. How Does an Assumable Loan Work?

Who is responsible for repaying an assumable mortgage?

An assumable mortgage is a loan that can be taken over, or assumed, by a qualified third party. After assuming the seller’s mortgage, the buyer becomes responsible for repaying the existing loan. The outstanding balance, mortgage interest rate, repayment period and other terms often don’t change.

How can I find out if my mortgage is assumable?

If there’s a home you’re particularly interested in, you or your agent may speak to the seller about their current mortgage loan. A quick call to the lender can confirm if the loan is assumable—and if you might be eligible to take it on.