What does it mean when a loan is non-conforming?

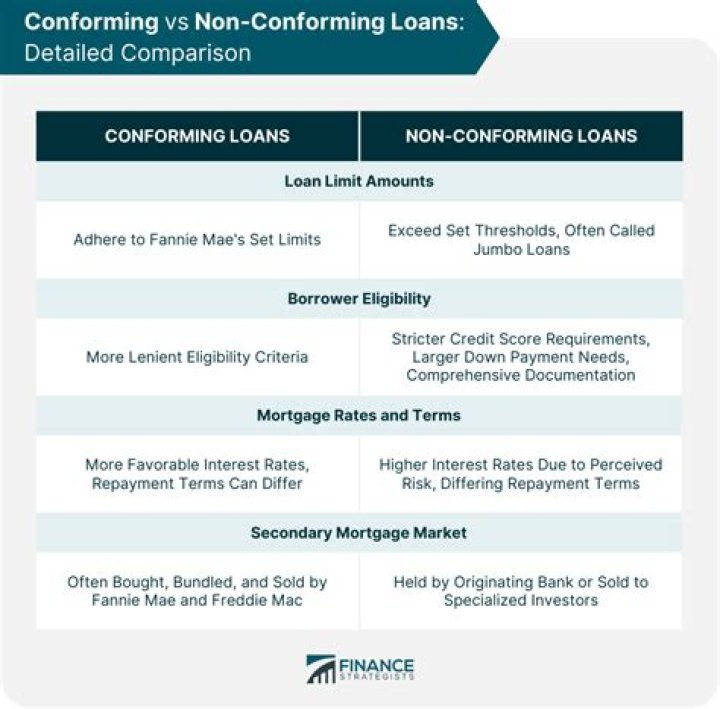

A non-conforming loan is a loan that doesn’t meet Fannie and Freddie’s standards for purchase. There are two main reasons why a loan might not conform: someone else can buy the loan or the loan is too large to be considered a conforming loan.

What is the best description for a non-conforming loan?

A nonconforming mortgage is a home loan that does not adhere to government-sponsored enterprises (GSE) guidelines and, therefore, cannot be resold to agencies such as Fannie Mae or Freddie Mac. These loans often carry higher interest rates than conforming mortgages.

Is a subprime loan a nonconforming loan?

There are many types of nonconforming loans. These include: A subprime loan. A jumbo loan with higher loan limits.

Is non-conforming same as jumbo loan?

Non-conforming loans are loans that cannot be purchased by Fannie Mae or Freddie Mac. Jumbo loans exceed the conforming loan limits and have different underwriting guidelines.

Is FHA a nonconforming loan?

A non-conforming loan is simply any mortgage that doesn’t conform to the requirements set forth by Fannie Mae and Freddie Mac. Non-conforming loans commonly include jumbo loans (those above Fannie Mae and Freddie Mac limits) and government-backed loans like VA loans, FHA loans or USDA loans.

What is another name for non-conforming loan?

Non-conforming loans are loans that aren’t bought by Fannie Mae or Freddie Mac. The most common types are government-backed mortgages – like FHA, USDA and VA loans – and jumbo loans.

Is a conforming loan the same as an FHA loan?

A conforming loan is one that adheres to the size limits used by Freddie Mac and Fannie Mae, the two U.S. corporations that purchase mortgage loans. So no, an FHA loan is not the same as conventional. They are two different things.

What’s the difference between a conforming and nonconforming loan?

A conforming loan meets the standards of Fannie Mae and Freddie Mac, mainly meeting the conforming loan limits. Nonconforming loans are government-backed home loans such as FHA loans; or jumbo loans, which exceed the maximum conforming loan limit.

Why are nonconforming mortgages so hard to sell?

Nonconforming mortgages are not bad loans in the sense that they are risky or overly complex. However, financial institutions dislike them because they are harder to sell since they do not conform to GSE guidelines. For this reason, banks will usually command a higher interest rate on a noncomforming loan.

Can you get a non conforming loan if you have a bankruptcy?

Because the lenders are private, any of the guidelines, except loan limit, are up to their discretion. For that reason, a non-conforming loan may be available even if you have had a bankruptcy. Conforming loans are made by banks and other financial institutions and backed by Fannie Mae and Freddie Mac.

Is there a down payment requirement for a non conforming loan?

Individual lenders set their own standards on qualifications and how much you can take out in a jumbo loan. Lower down payment requirements: Non-conforming government-backed loans usually have lower down payment requirements than conventional loans. You can buy a home with 0% down if you qualify for a USDA or VA loan.