What are the characteristics of a universal life insurance policy?

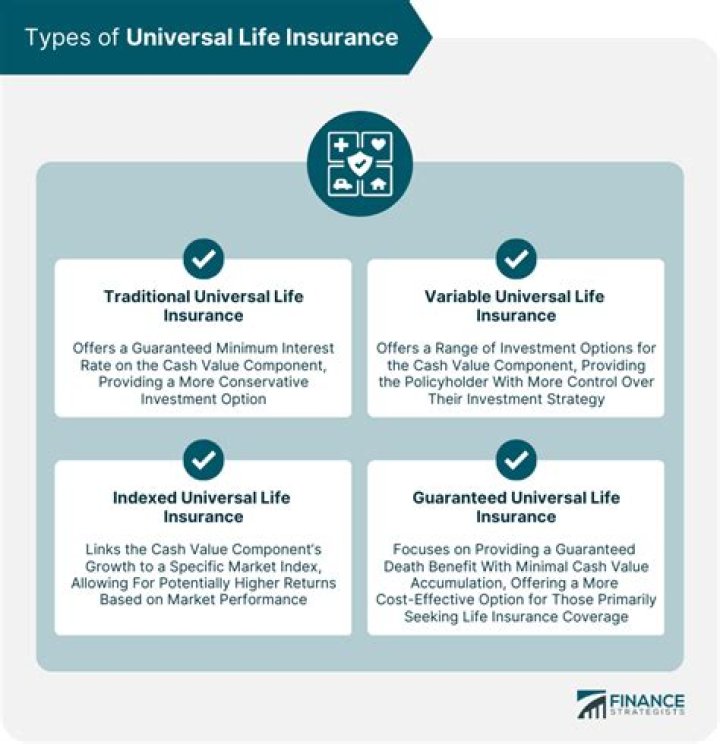

Universal life insurance offers lifelong coverage, provides flexibility when it comes to paying premiums and choices for how the policy’s cash value is invested. A standard universal life insurance policy’s cash value grows according to the performance of the insurer’s portfolio and can be used to pay premiums.

What are the characteristics of life insurance explain?

Term life insurance is pure insurance protection that pays a predetermined sum if the insured dies during a specified period of time. 2 On the death of the insured person, term insurance pays the face value of the policy to the named beneficiary. All premiums paid are used to cover the cost of insurance protection.

What do you need to know about universal life insurance?

Universal life insurance is permanent life insurance that has an investment savings element and low premiums. Most universal life insurance policies contain a flexible premium option. A policyholder will pay taxes on any withdrawals they make from the excess cash value of the universal life insurance plan.

Are there flexible premiums for Universal Life Insurance?

Universal Life Flexible Premiums. Although there is flexibility with premium remittance, policyholders must be attentive to the rising cost of insurance and plan accordingly. Depending on the credited interest, there may not be enough cash value to keep the policy in force, thus requiring higher premium payments from the policyholder.

What’s the difference between Universal Life and whole life?

It is important to note that, while whole life has a fixed premium, universal life does not. It can continue to increase throughout the lifetime of the policy. The savings in your policy can be used as collateral if you choose to borrow money from the insurance company against the accumulated cash value without tax implications.

What are the tax implications of universal life insurance?

Unlike term life insurance, a universal life insurance policy can accumulate cash value. There are no tax implications for policyholders who borrow against the accumulated cash value of their policy. As the name implies, the cost of insurance is the minimum amount of a premium payment required to keep the policy active.