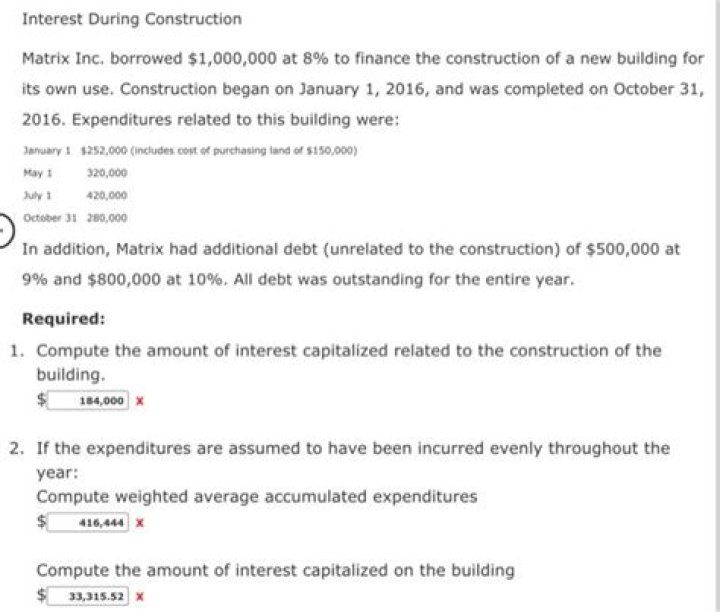

How might you finance the construction of a private home?

On a construction-to-permanent loan, you can work with the private-money lender for the construction and then with one of your correspondent lenders to do a rate-and-term refinance out of the hard-money loan. The private lender will require a 20 percent nonrefundable deposit, which can be rolled into the takeout loan.

Can you finance the construction of a house?

You can get an end loan if construction is complete on the home. One good aspect of an end loan is that the mortgage application for a newly constructed home is the same as it is for any other home. Less complicated is always appreciated when it comes to financing applications.

What is the best way to finance new home construction?

FHA Loans. If you’ve got only minimal cash to make a down payment and your credit history has a few blemishes, a federal government-backed loan is most likely your best choice. FHA (Federal Housing Administration) loans allow down payments as low as 3.5 percent along with generous credit underwriting.

How does finance work when building a house?

Construction loans offer progressive drawdown, meaning the lender pays your loan in small chunks – as and when your builder completes a stage – rather than in a lump sum. Most construction loans are interest-only for the duration of the build too, so while your home is being built, your costs are kept to a minimum.

What’s the best way to finance a home construction?

The second option is a two-time close loan. You will get a loan for the construction, and then you will get another standard loan for the mortgage. Take note, once construction is complete, you are in fact refinancing the mortgage. This means you will need to reapply to get approved for the loan and you must pay closing costs again.

How does a construction loan for a house work?

What is a construction loan? A construction loan is short-term or temporary financing that funds your home build and is paid out through a series of installments as the construction advances. Construction loans are considered riskier than standard home loans, since no house exists that the lender can secure as collateral.

What kind of loan do you need to build a house?

Most owners secure two loans, one for each period. The first is the period during construction, funded with a construction loan. The second is the period after construction, funded with a permanent loan, AKA a takeout loan.

When do you pay off your construction loan?

When your home is completed, you pay off the construction loan with permanent financing (i.e. your mortgage). You might enjoy 8 Savvy Ways to Stay on Budget when Building a House. Also referred to as One-Time-Close Construction Loan, the Construction-to-Permanent Loan is the more popular option.