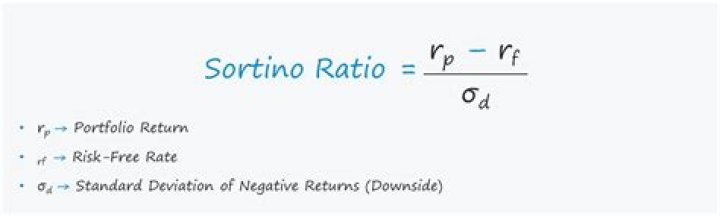

How is Sortino ratio calculated example?

The downward deviation is used for Sortino ratio calculation, whereby it considers only those periods when the rate of return was lower than the target or risk-free rate of return….and the Sortino ratio can be calculated using the formula:

- Soriano Ratio Formula = (Rp-Rf)/ σd.

- Sortino ratio = (7% – 6%)/4.81%

- = 0.2.

What is a good Sortino ratio?

A Sortino ratio greater than 1.0 is considered acceptable. A Sortino ratio higher than 2.0 is considered very good. A Sortino ratio of 3.0 or higher is considered excellent.

How do you calculate downside deviation?

Calculate the square root of your result. Multiply that result by 100 to calculate the investment’s downside deviation as a percentage. Concluding the example, calculate the square root of 0.000567 to get 0.0238. Multiply 0.0238 by 100 to get a 2.38 percent downside deviation.

Where is the Sortino ratio in Excel?

Sortino Ratio = (r – rf) / σd Where, r: Expected Return. rf: Risk-Free Rate of Return. σd: Standard Deviation of Negative Assets Return / Downside Deviation.

Is Sharpino or Sortino always higher?

Just like the Sharpe ratio, a higher Sortino ratio result is better. When looking at two similar investments, a rational investor would prefer the one with the higher Sortino ratio because it means that the investment is earning more return per unit of the bad risk that it takes on.

What is a good information ratio?

The higher the information ratio, the better. Generally speaking, an information ratio in the 0.40-0.60 range is considered quite good. Information ratios of 1.00 for long periods of time are rare.

Is a higher Sortino ratio Better?

How is downside risk measured?

At an enterprise level, the most common downside risk measure is probably Value-at-Risk (VaR). VaR estimates how much a company and its portfolio of investments might lose with a given probability, given typical market conditions, during a set time period such as a day, week, or year.

What is the formula for the Sortino ratio?

The formula for calculating the Sortino ratio is: Sortino Ratio = (Average Realized Return – Expected Rate of Return) / Downside Risk Deviation The average realized return refers to the weighted mean return of all the investments in an individual’s portfolio.

Which is better the Sortino ratio or the risk adjusted ratio?

In contrast, the Sortino ratio examines risk-adjusted returns, but it only considers the downside risks. In such a way, the Sortino ratio is seen as a better indicator of risk-adjusted returns since it doesn’t consider upside risks, which aren’t a cause for concern to investors.

Is the Sortino ratio the same as the Sharpe ratio?

The Sortino Ratio was developed as a commercial measure by the investment industry, and does not have the academic heritage and strict mathematical definition of the Sharpe Ratio. As such, several methods are commonly used to measure downside risk, including the semi standard deviation, or the square root of the 2nd lower partial moment.

What is the Sortino Ratio for a mutual fund?

If the mutual fund’s 2019 figures include an annualized return of 24% and a 20% downside deviation, and the risk-free rate is 5%, what is the fund’s Sortino ratio for 2019? Let’s break it down to identify the meaning and value of the different variables in this problem.