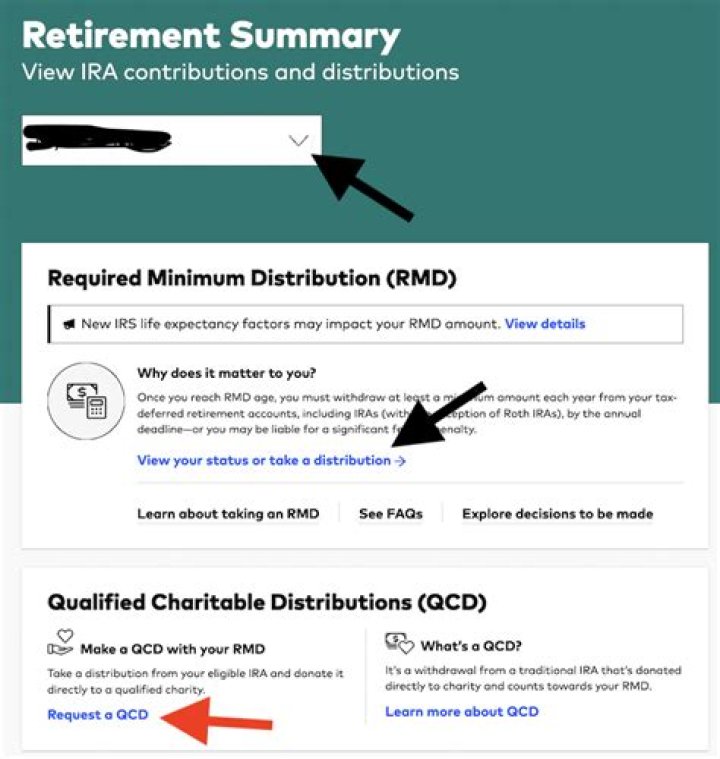

Do I have to take RMD from 457 if still working?

If you’re still working at 70½, you may not need to take RMDs from your current employer’s 457 plan until you retire, but you still need to take RMDs from former employers’ plans and traditional IRAs.

What are the RMD requirements for 2021?

You reach age 70½ after December 31, 2019, so you are not required to take a minimum distribution until you reach 72. You reached age 72 on July 1, 2021. You must take your first RMD (for 2021) by April 1, 2022, with subsequent RMDs on December 31st annually thereafter.

Are pension plans subject to RMD?

WHAT KIND OF RETIREMENT ACCOUNTS HAVE RMDs? RMD rules apply to traditional IRAs and IRA-based plans such as SEPs, SARSEPs, and SIMPLE IRAs. They also apply to all employer-sponsored retirement plans, including profit-sharing plans, 401(k) plans, 403(b) plans, and 457(b) plans.

Are deferred annuities subject to RMD?

Required minimum distribution (RMD) is the IRS-mandated minimum annual withdrawal amount from tax-deferred retirement accounts for participants aged 70 ½ or 72, depending on the year they were born. Annuities held inside an IRA or 401(k) are subject to RMDs.

Do I have to take an RMD from an annuity?

Qualified variable annuities held in IRAs are subject to the IRS required minimum distribution (RMD) requirement. At age 72, qualified account owners are required to begin taking RMDs from their IRAs. A 50% penalty on the RMD amount may be assessed if not taken as required.

When do you have to take a 457 distribution?

Required Minimum Distribution – You are required to start taking distributions when you reach age 72. The SECURE Act recently changed the age for the initial Required Minimum Distribution from 70 ½ to 72. Your 457 (f) plan is heavily influenced by both 409A and 457 standards.

Can a non governmental organization offer a 457 plan?

Non-governmental or 501(c) organizations can also offer eligible 457(b) plans, but only to certain “highly compensated employees.” In addition, assets in these plans are not held in trust but remain with the employer until distribution. The rollover privileges are much more restricted, too.

What kind of retirement plan is a 457 plan?

A 457 plan is one of a number of retirement plans that employers offer to their workers, but it is less common and more complex than a 401 (k) or 403 (b). Most private companies usually offer 401 (k) plans and public school systems, and other nonprofits offer 403 (b) plans.

Is there a penalty for early withdrawal from a 457 plan?

Distributions are taxable, but unlike other employer-sponsored plans, there is no penalty for early withdrawals from a 457 plan. Because 457 plans are complex, it’s wise to talk to a financial advisor or tax-planning expert before you retire.