Do adjusting entries only affect balance sheet accounts?

Adjusting entries affect only balance sheet accounts. The accounting principle that requires revenue to be recorded when earned is the: Revenue recognition principle. Adjusting entries result in a better matching of revenues and expenses for the period.

What are the effects of the income statement and balance sheet if adjusting entries are not made?

If the adjusting entry is not made, assets, owner’s equity, and net income will be overstated, and expenses will be understated. While most expenses are prepaid, a few are paid after a service has been performed.

What affect both the balance sheet and income statement?

Liabilities are what you owe and include accounts payable, accrued expenses, bank debt and credit card bills. For example, if expenses are coded as an asset on the balance sheet when it should be included on the income statement, it can affect both reports; i.e. the income statement would be overstated.

How do adjusting entries affect financial statements?

Impact on the Income Statement Adjusting entries aim to match the recognition of revenues with the recognition of the expenses used to generate them. A company’s net income will increase when revenues are accrued or when expenses are deferred and decrease when revenues are deferred or when expenses are accrued.

What are the rules for adjusting an income statement?

Because an adjusting entry involves the income statement, it must include: At least one expense or revenue account Adjusting entries: 1) Affect at least one Income Statement account 2) Affect at least one Balance Sheet account 3) Involve at least one revenue or expense account 4) Involve prepaid expenses or accruals

How many accounts are affected by an adjusting entry?

All adjusting entries affect at least: One Balance Sheet and Income Statement account Because an adjusting entry involves the income statement, it must include: At least one expense or revenue account Adjusting entries: 1) Affect at least one Income Statement account 2) Affect at least one Balance Sheet account

How many accounts are involved in adjusting a balance sheet?

One Balance Sheet and Income Statement account Because an adjusting entry involves the income statement, it must include: At least one expense or revenue account Adjusting entries: 1) Affect at least one Income Statement account 2) Affect at least one Balance Sheet account 3) Involve at least one revenue or expense account

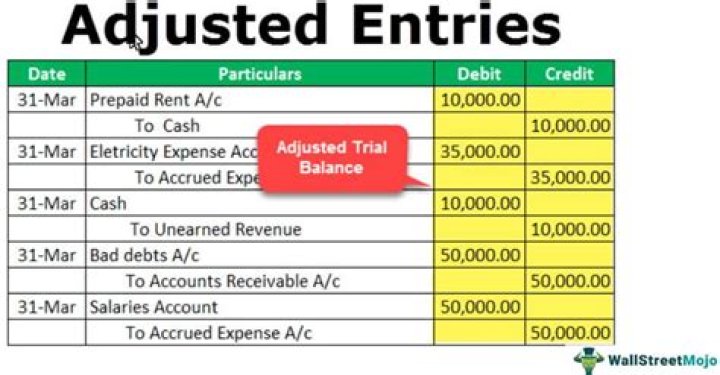

When to adjust entries in a financial statement?

With respect to when adjusting entries are made during the accounting cycle, they will be made after the unadjusted trial balance and before the company prepares its financial statements, bringing the amounts in the general ledger accounts to their proper balances.