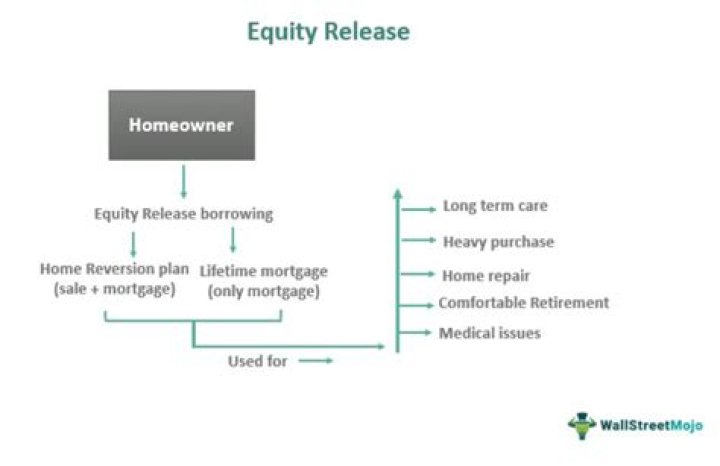

Can you have a mortgage and equity release?

Whether you currently have a repayment mortgage or an interest-only mortgage, it is required to be repaid as part of the equity release process. Upon completion of your equity release, it will be the equity release lender that has the first charge on your property, replacing your existing mortgage lender.

Do I have to pay off my mortgage to get equity release?

Three tips for how to pay off a mortgage with equity release You must be able to pay off any current mortgage or debt secured against the property by completion – either with the proceeds of the lifetime mortgage or other savings you may have.

What happens to your mortgage when you release equity?

Most people who take out equity release use a lifetime mortgage. Usually you don’t have to make any repayments while you’re alive. Instead, interest is ‘rolled up’, which means the unpaid interest is added to the loan.

Can you release equity during fixed term mortgage?

If you want to remortgage to release equity you will need to contact your current mortgage company or remortgage with a new lender in order to release the cash. With mortgage rates relatively low, remortgaging may seem like the cheapest way to borrow large sums of money.

What are the drawbacks of equity release?

The main disadvantage of equity release is that it does not pay you the full market value for your home. You will receive far less money than you would from selling the property on the open market – although of course in that situation you would still have to find somewhere else to live.

How can I release equity from my home?

If you are looking to release equity from a home you have not completely paid off, you will be required to use the funds you secure to pay off the remainder of the mortgage as this is one of the terms and conditions of equity release. Any excess money remaining after the mortgage has been completely paid will be yours to spend how you please.

Do you have to pay interest on equity release?

You don’t need to have fully paid off your mortgage to do this. As a rule, you can take the money you release in one lump sum, in several smaller amounts on which you’ll pay interest, or as a combination of both. Yet make sure you do it in the right way as if you get it wrong, it can prove expensive, as these tweets show:

How old do you have to be to get equity release on a house?

Indeed as long as the qualifying criteria of the equity release scheme can be met which is a minimum age of 55 & the loan can be raised based on this property value and the age of the youngest applicant. In such circumstances, equity release can be used in the same way as any conventional mortgage is used towards a house purchase.

What happens to your estate when you release equity?

There are certain ways in which equity release can reduce the amount of IHT due on a homeowner’s estate due to the way different types of assets are taxed. By releasing equity in your property, you are effectively reducing the value of your property – potentially to a value below the £325,000 IHT threshold.