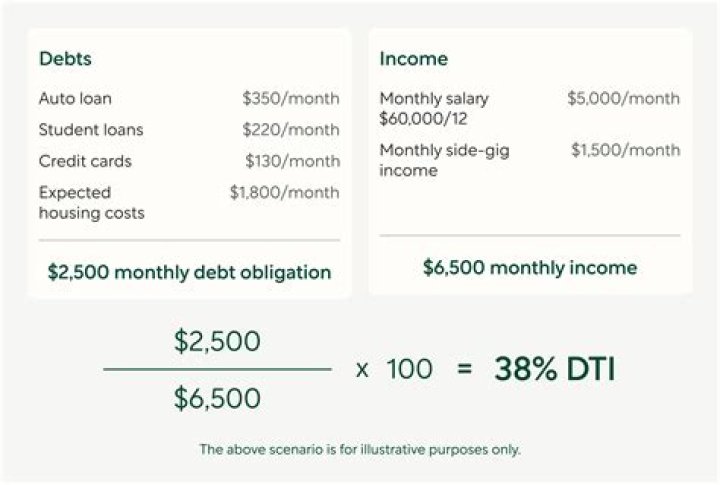

Can I get approved for a mortgage with high debt-to-income ratio?

There are ways to get approved for a mortgage, even with a high debt-to-income ratio: Try a more forgiving program, such as an FHA, USDA, or VA loan. Restructure your debts to lower your interest rates and payments. Get a lower mortgage rate by paying points to get a lower interest rate and payment.

What is the highest debt-to-income ratio a home buyer can have and still qualify for a mortgage?

43 percent

Evidence from studies of mortgage loans suggest that borrowers with a higher debt-to-income ratio are more likely to run into trouble making monthly payments. The 43 percent debt-to-income ratio is important because, in most cases, that is the highest ratio a borrower can have and still get a Qualified Mortgage.

What’s the highest debt to income ratio you can get?

However, some lenders will accept a higher-debt-to-income ratio because of an exemption in the rule if the lender can prove by other means that the consumer would be able to make payments on the mortgage. The highest debt-to-income ratio quoted by lenders who will consider high debt-to-income ratios is currently 50%.

Can you get a mortgage with a 43 percent debt to income ratio?

There are some exceptions. For instance, a small creditor must consider your debt-to-income ratio, but is allowed to offer a Qualified Mortgage with a debt-to-income ratio higher than 43 percent.

What’s the highest DTI ratio you can get for a mortgage?

As a general guideline, 43% is the highest DTI ratio a borrower can have and still get qualified for a mortgage. Ideally, lenders prefer a debt-to-income ratio lower than 36%, with no more than 28% of that debt going towards servicing a mortgage or rent payment. 2

How can I lower my debt to income ratio?

Although this may help you get approved for credit, it won’t actually lower your personal debt-to-income ratio. The other way to improve your debt-to-income ratio is to lower your debt levels: Stop taking on more debt. Don’t apply for new credit, avoid running up your credit card balances, and delay any major purchases. Pay down existing debt.